Household Budgeting

It's not easy to keep track of what you spend each month. Creating a monthly budget is important so that you know how much money you have and how you are spending it.

A household budget includes income, or the money you have available each month. It also includes expenses, or the things you pay for.

A budget will help you to decide how to spend your money. If you run into difficulties, a budget can also help you make changes to your spending. A budget helps to:

- pay for your living expenses;

- decide what is most important to spend money on;

- manage our debts; and,

- prepare for unexpected bills or emergencies.

Making a budget is something we all need to do. There is no magic formula – it is simply getting the most from the money we have.

Building a budget is a step-by-step process. The following sections will help you to create and manage a monthly budget:

1. Budgeting

What is a Budget?

A budget is a plan on how you spend your money. It includes income, or the amount of money you have available each month. It also includes expenses, or what is spent each month.

A budget helps you decide how to spend your money and how to change spending if you need to. A budget is important for everyone, especially when:

- we may be behind in paying bills, such as rent or utilities, or paying off debt;

- we want to make the most of our money but are not clear how much we are spending on what kinds of things; or

- we want to plan for certain purchases, unexpected bills or emergencies.

Making a Budget

The first step of making a budget is to keep track of the money received and where that money comes from. This includes all money from a job and federal and provincial benefit programs (e.g. Employment Insurance, Canada Child Benefit, Goods and Services Tax Rebate Program, etc.).

Second, keep track of monthly expenses and list them. This includes rent, utilities, groceries and other regular payments you need to make.

Subtract these expenses from your income.

If expenses are greater than your income, you may need to:

- find areas to cut back or reduce spending; or

- look for ways to increase your income.

If your income is more than your expenses, you should try to save some money for unexpected bills or emergencies.

Example of a budget

| Your Income | Your Expenses | ||

| Earned Income | $1,600 | Rent | $1,100 |

| Canada Child Benefit | $540 | Utilities | $250 |

| Total Income | $2,140 | Groceries | $575 |

| Insurance | $56 | ||

| Transit | $75 | ||

| Total Expenses | $2,056 | ||

| Total Remaining Budget |

$84 | ||

Needs and Wants

If you think you need to change your spending habits, it is important to think about what you "need" and what you "want."

Some "needs" include:

- housing and food costs;

- things for work, such as travel or clothing;

- heat, water and power; and

- costs related to having children.

Some "wants" include:

- entertainment costs;

- eating out; and

- electronics we don't really need.

Understanding needs and wants will help you to manage within your monthly budget.

How to create a budget summary that outlines your income and expenses

Download the Budget Summary Worksheet and enter your income and expenses. The income section includes spaces to enter all the types of income you may get. Be sure to enter your net income (income after all deductions have been made). The expense section is divided into four categories. Not all may apply to you, but fill out what you know.

At the bottom of the worksheet, your net income is the total of all your income, and your net expenses is the total of all your expenses. In the "net gain/loss" area:

- If your total is not in brackets, your income is higher than your expenses. You may want to think of ways to save for the future.

- If your total is in brackets, your expenses are higher than your income. You may need to think of ways to reduce or cut some of your expenses. The Wants and Needs Calculator may help with this.

Tips for Increasing Income

- Completing your income taxes each year makes sure you get all federal and provincial benefits you are eligible for. This includes Goods and Services Tax Credit, Canada Child Benefit, Canada Pension Plan, etc.

- Continue to look for improved employment opportunities to increase your monthly income. Consider steps to get a better job, including career counselling, training or education programs. For more information, please visit Labour Market Services.

Tips for Lowering Costs

- Budget for current expenses and any debt or outstanding payments you need to make. If you are behind on a utility, for example, try to pay your current amount plus a portion of what you owe. Contact your utility provider to make sure they are aware you have a plan and discuss options with them.

- Cut down on the biggest expenses when you can. Cut back on utility use by turning off lights, lowering your thermostat overnight or when not at home. Contact your utility company to see what tips they can offer, or visit these websites for tips:

- Be very selective when looking for new accommodations. Understand the total housing cost (i.e. rent and utility amounts). For more information on social housing, please visit the Saskatchewan Housing Corporation.

- Cut back on cable, internet and cellphone plans. Look for apps that offer free messaging and long-distance calling. Contact your service provider and ask how payments can be lowered.

- Reduce food costs by purchasing in bulk. Use grocery stores that have lower mark ups and use coupons to save money.

- Determine the amount you can spend on groceries. Paying with cash can help to ensure you do not overspend. Credit cards are convenient, but they have high interest rates and, if not paid on time, will cause greater debt.

How to reduce your expenses

Use the Wants and Needs Calculator to help think of ways to reduce or cut expenses.

To use the calculator, enter the cost of an item in the 'cost' column, and the number of times per month you spend this amount in the 'frequency' column. The result is how much you spend a month on a particular item. For example, if your 'cost' for eating out is $15, and the 'frequency' is 15 times a month, the monthly cost is $225. If you reduce eating out to 5 times a month, your monthly cost is $75. Cutting down on the number of times you eat out each month saves you $150.

2. Housing

Rent or mortgages are regular payments everyone needs to make. This includes paying taxes and insurance.

How much can I afford?

To make sure your housing fits your budget, consider some of the following:

- Live in a place that has the right amount of space that is needed. Don't pay for extra space that you don't use.

- Live close to work because it may help lower costs of getting to work.

- To help with rent or mortgage costs, consider finding a roommate. If renting, check your rental agreement or with your landlord to see if other people can live with you.

- Check with the Saskatchewan Housing Corporation (SHC) for low-income rental options.

What if I run into problems?

Sometimes, it may be hard to make mortgage or rent payments on time. If this happens, there are some things that can be done.

If you have a mortgage:

- Contact your bank to see what options are available. Some mortgage agreements allow people to skip a payment, although this payment will still need to be made up later. Contacting the bank right away may make the difference between keeping or losing a home.

If you rent:

- Contact your landlord to see what payment options are available. Late rent payments can lead to eviction. Talking to your landlord right away is important.

- Explain your situation to your landlord so they know it is temporary.

- Some landlords will allow part of a payment when the rent is due, and the rest a few days later. Ask your landlord if this is possible.

Security Deposits

Most landlords ask for a security deposit. In Saskatchewan, landlords can charge a security deposit equal to one month's rent. Some landlords may ask for half of the security deposit when the rental agreement is signed and the rest within two months of moving in.

When you move out, your landlord should inspect the apartment with you:

- Landlords must return a security deposit if the apartment is clean and undamaged. They must return the security deposit within seven days.

- Landlords can keep a security deposit if the apartment is not clean or has damage. They can also keep it if you do not pay the rent owed. Landlords who keep a security deposit have to let you know about it within seven days.

It is important to have a security deposit returned when moving because this money can be put towards the security deposit on a new place. The security deposit is your money and if you need assistance with having your landlord return it, please see the information below on the Office of Residential Tenancies.

The Office of Residential Tenancies (ORT) is an agency that works outside government. They provide information on landlord and tenant rights and responsibilities.

If landlords or tenants cannot settle a dispute, they both have the right to ask the ORT to help settle it.

3. Transportation

Make sure to think about transportation costs when making a budget. If you own a vehicle, this includes gas, repairs and insurance.

Some tips to consider:

- Use the local bus to save on gas and parking costs. It can also save on vehicle repair costs.

- Avoid taking taxis when possible. Taxis are convenient but cost more. A round trip taxi ride within the city can cost 150% or more than taking the bus.

- Share a ride with a friend or co-worker.

- Live close to work to save on the cost of getting there.

- If you have a car, take care of it and perform regular maintenance.

- Some communities have volunteer driver programs for people with health issues who need regular treatment. Check with volunteer services at your local health care centre for information.

If you receive income support from the Ministry of Social Services, you can get a discounted bus pass in Regina, Saskatoon, Prince Albert, Moose Jaw, North Battleford, Swift Current and Yorkton.

4. Power, Heat and Water

It is important to pay power, heat and water bills on time.

Falling behind on these bills can result in having services reduced or turned off. It can cost more to have them turned back on.

Planning for these Costs

Apartments sometimes include heat and water with rent. Power may be a separate cost. Ask your landlord what is included in your rent.

Homeowners pay their own power, heat and water. Some of these costs may be higher than others because of the size or age of the home.

How you can budget for these costs

- Review your bills to see if they are higher at certain times of the year. Try to use less during these times.

- SaskPower and SaskEnergy offer equalized payment plans. The yearly cost is averaged over 12 months into "equalized" monthly payments. At the end of 12 months there may be a "settle-up" payment if actual monthly use was higher or lower than the equalized payment.

- Read your meter once a month and phone in your usage if your bills indicate they are estimates.

- Take small steps to reduce costs. Close or seal windows in winter. Turn down the temperature on the hot water heater.

- Be aware when power, heat and water costs are increasing. In Saskatchewan, these increases are announced before they take effect. Knowing this can help you choose to reduce the amount of power, heat or water used.

- You can contact your power, heat or water provider to see what options there are if you fall behind on payments.

- To help with these payments, save money by cutting back costs in other areas, such as cable or internet.

When you move

- Contact your utility providers and disconnect power, heat and water or have your name removed from the account. Not doing so can lead to additional charges in your name.

- Ask about re-connect charges or outstanding amounts that need to be paid before getting power, heat and water hooked up in your new place.

More Information

- For water and sewer questions, contact your local city or town office.

- For questions and information about your heating bill, contact SaskEnergy customer service at 1-800-567-8899. You can also open an online account at account.saskenergy.com.

- For questions and information about your power bill, contact SaskPower customer service at 1-888-757-6937. You can also open an online account at mypoweraccount.saskpower.com.

Alternative Heating Sources

Alternative heating sources include wood, oil and propane.

Typically, these costs are higher at certain times of the year. In spring through fall, it is important to put money aside as bills in the winter months will increase so you will need to increase the amount of your payment at that time.

Contact your provider to see if they will set up a monthly payment instead of a once a year payment.

5. Food Costs

Always include food costs in your monthly budget. This is also an area where we can lower what we spend.

Tips to lower food costs include:

- Eat at home rather than eating out. Eating a meal out costs over twice as much as making a meal at home.

- Purchase items, such as pasta or rice, in bulk. Buying in bulk is usually cheaper than buying small quantities.

- Make a shopping list and stick to it. This can help avoid buying things that are not needed.

- Pay with cash rather than a credit or debit card to reduce impulse buying.

- Use grocery stores that have lower mark ups and use coupons to save money.

6. Cable, Internet and Phone

Cable and internet are great ways to learn, communicate and be entertained. But how much of these things do we actually need?

Many people pay for more of these services than they actually use. When making a budget, this is one area that is easy to cut back on.

Some tips for saving money:

- Getting rid of premium and high definition channels can save $20 or more each month.

- Getting rid of PVR services can save $10 or more each month.

- Bundling cable and Internet services is often cheaper. Check for competitive rates.

- Reduce Internet speed – we sometimes have higher download speeds than we need.

Phone

A phone is something we need, but are we paying for services we don't use? Phone services are another area you can save money when making a budget.

Some tips for saving money:

- Most people don't need both a home phone and cell phone. Choose which works the best for you and get rid of the other.

- Use cell phone apps that allow free long distance calling.

- Choose a cell phone plan wisely. You can waste money if you have services you don't use.

- Use Wi-Fi to reduce data charges.

- Use family plans to share and save on costs.

- The latest device is nice to have, but costs money. If your current phone works, take care of it and hold onto it longer.

- Search for cheaper services.

7. Banking

Opening a Bank Account

You can open an account at a bank or credit union with the right identification (ID). The types of ID required usually include any of the following:

- Driver's licence

- Current Canadian passport;

- Canadian birth certificate;

- Social Insurance Number;

- Certificate of Indian status; or

- Provincial health card.

People who are not Canadian citizens need to provide documents explaining their current status.

Contact the bank or credit union to know which ID they require.

Before opening a bank account:

- Consider using the account for paying bills (i.e. power, heat or water). This is a great way to set up easy to manage and scheduled bill payments.

- What fees will the bank charge? Fees are different depending on the type of account you have. Make sure you choose an account with the lowest fees.

- Do you understand the bank's terms and conditions? Ask the bank questions if you do not understand something. Keep a copy of your account agreement.

Once you have an account:

- Review your monthly statements. You do not want to pay more fees than you are supposed to, or be charged for items you did not buy.

- Review your account from time to time to make sure it meets your needs. Switch banks if you feel another bank provides lower fees or better services.

How to keep your identity safe

Identity theft can happen to anyone. You can do a few simple things to keep yourself safe:

- Keep your banking details, such as the PIN for your debit or credit card, safe. Do not share or give anyone this information.

- Do not give people your Social Insurance Number or other identification. Others can use this information to open bank accounts or credit cards in your name.

- Keep bank and credit card statements in a safe place. Shred them if they aren't needed.

- If you lose your debit or credit card, immediately contact your bank. Some online banking apps allow you to freeze or hold your accounts. Check with your bank for more information.

- Keep your devices, such as your cellphone or computer, password protected. This will keep your online banking safer.

- Check your accounts for purchases or withdrawals you did not make. Contact your bank immediately if you notice something wrong with your account.

- If you keep cash, keep it secure or hidden.

8. Credit Cards and Payday Loans

Credit Cards

Credit cards allow you to borrow money to buy things. They are usually issued by banks, who charge interest and fees on the money you borrow.

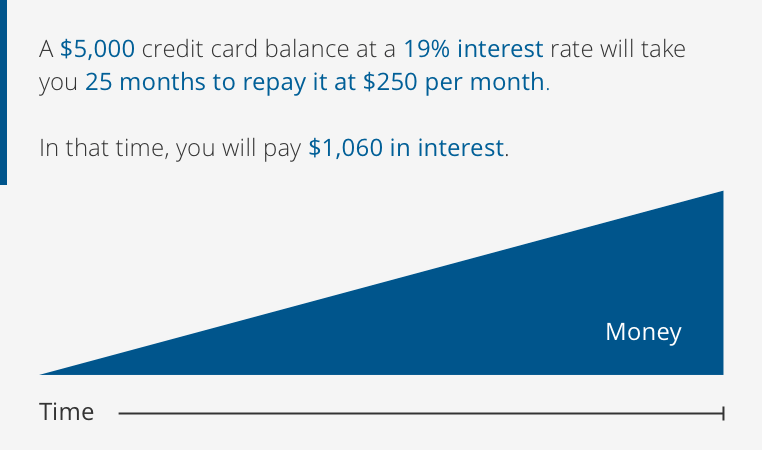

Credit cards usually have interest rates of between 18% and 22%.

While credit cards are a convenient way to pay for things, they have some downsides:

- If we are not careful with them, we can easily dig ourselves into debt.

- We can spend too much because of how easy they are to use.

- If we miss payments, the interest will make our debt grow higher.

Paying with cash usually helps us stick to a budget. If you do have a credit card:

- Understand what the interest rates and fees are. Credit cards can start with a low interest rate that increases after a few months.

- Pay off the total amount each month. This means not overspending with it.

- Avoid using credit cards to take cash out of the bank. This can make debt increase quickly.

- Do not use a credit card to buy things that are not affordable.

Payday Loans

Payday loans are offered by money lenders or local cheque-cashing places. They offer advances on a person's next pay cheque.

Payday loans charge high interest rates or fees on the amount borrowed. These rates apply to the length of the loan.

If you take out a $400 loan for two weeks and the fees are $20 for every $100 borrowed, at the end of two weeks you will owe $480. If this amount remains unpaid for a year, the amount owed will be over $2,000 because of the fees.

Payday loans are not a good option for borrowing. They can leave you deep in debt. Always look for better options such as borrowing from a family member or friend, or working with your landlord and utility providers on a plan to slowly pay down your debt and ensure you are making payments on all of your bills.

If you run into difficulties

Owing money on credit cards all the time is a problem. Because of interest charges, debt can grow and become hard to manage. Avoid:

- using a credit card out of necessity;

- using a credit card for daily living expenses;

- missing multiple payments or due dates;

- carrying a balance near the card maximum; and

- borrowing from one card to pay down other debt.

Do not ignore debt. Instead, consider taking the following actions:

- Look for ways to increase income.

- Make a budget that is easy to stick with. Reduce "wants" or things we don't really need.

- Use savings to pay down debt. Make sure to have money for emergencies.

- Contact your bank to see if you can set up a different payment schedule or interest rate.

- Seek credit and debt counselling options. Some organizations who may help include: